在建立通用线性模型时,当模型参数即斜率值绝对值过大时,容易存在过拟合的风险。可通过下面介绍的3种正则化方法将每个预测变量的斜率参数缩小为0或者接近0。

$$

y = \beta_0 + \beta_1x_1 + \beta_2x_2 + …+\beta_kx_k + \epsilon

$$

1、三种正则化方法#

线性回归最小二乘法损失函数:MSE

如下公式表示在一组给定的参数值模型中 所有预测值与观测值的差值的平方和(残差和,RSS):

$$

J = \sum_{i=1}^n(y_i-\hat{y_i})^2

$$

1.1 岭回归#

在上述RRS损失函数公式中,添加L2范数(所有斜率值的平方和)。可通过λ参数控制惩罚的强度。

$$

J=\sum_{i=1}^n(y_i-\hat{y_i})^2 + \lambda \sum_{j=1}^p{\beta_j^2}

$$

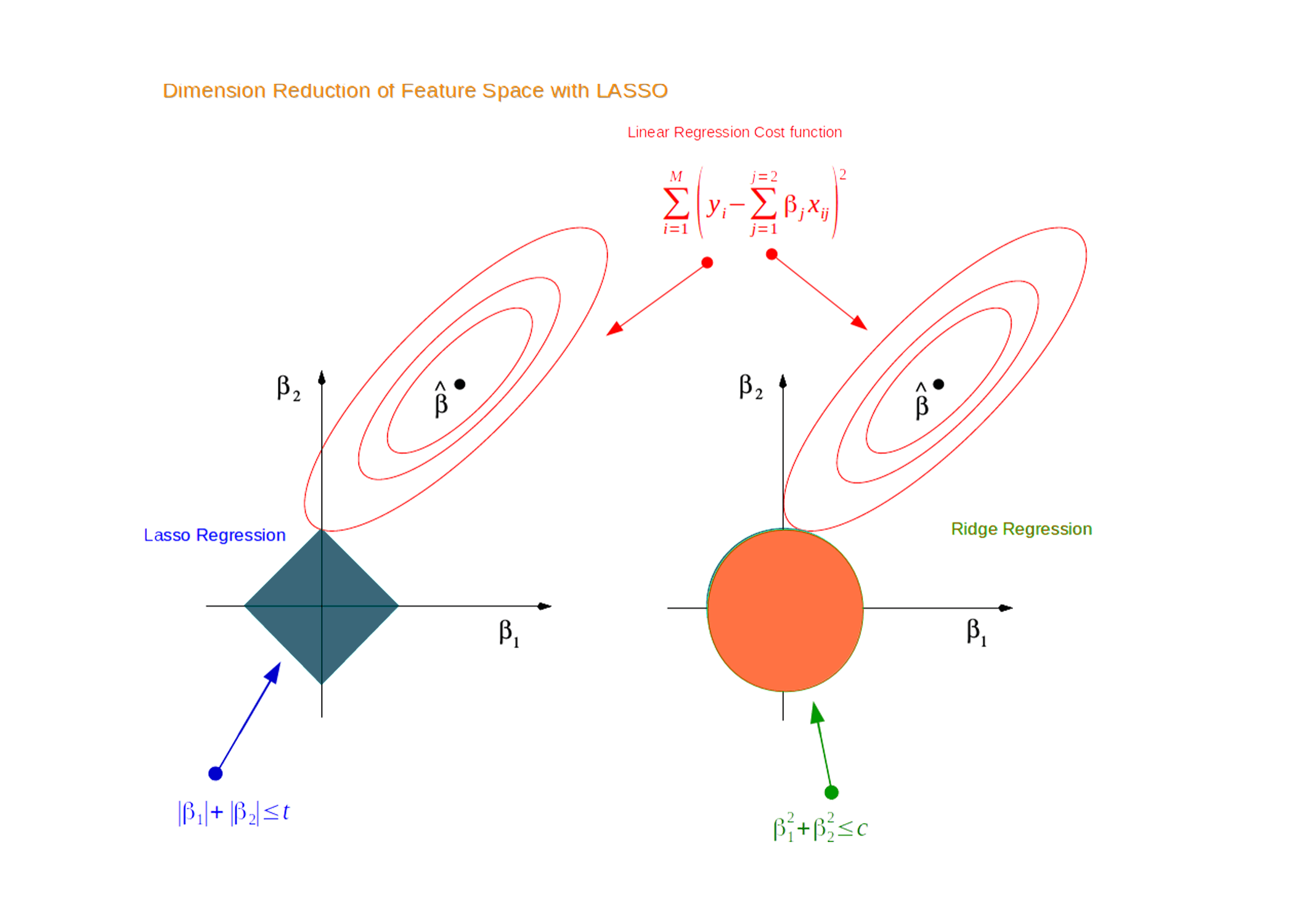

可结合下图理解:假设有两个预测变量,即有两个斜率参数。

(1)绿色圆表示不同参数值组合的MSE,中心值最小,越往外越大,黑色边表示相同MSE的等高线。

(2)蓝色圆边表示具有相同L2结果的不同参数值[r^2=β1^2+β2^2],总会存在一组参数值对应的RSS最小(如下图所示)。

1.2 LASSO回归#

在上述RSS损失函数公式中,添加L1范数(所有斜率值的绝对值和)。可通过λ参数控制惩罚的强度。

$$

J=\sum_{i=1}^n(y_i-\hat{y_i})^2 + \lambda \sum_{j=1}^p{|\beta_j|}

$$

可结合下图理解:假设有两个预测变量,即有两个斜率参数。

(1)红色同心圆表示不同参数值组合的MSE,中心值最小,越往外越大,黑色边表示相同MSE的等高线。

(2)蓝色正方形边表示具有相同L1结果的不同参数值[r=|β1|+|β2|],总会存在一组参数值对应的RSS最小(如下图所示)。

1.3 弹性网络#

(1) 岭回归与LASSO回归比较#

-

如上公式岭回归与LASSO回归的最主要差异在于惩罚项L2范数与L1范数的区别。

$$

J_{L2}=\sum_{i=1}^n(y_i-\hat{y_i})^2 + \lambda \sum_{j=1}^p{\beta_j^2}

$$

$$

J_{L1}=\sum_{i=1}^n(y_i-\hat{y_i})^2 + \lambda \sum_{j=1}^p{|\beta_j|}

$$

-

当λ=0时,等价于不加入惩罚项,取一组参数值使RRS值最小即可;

-

当λ>0时,岭回归加入了L2范数,LASSO回归加入了L1范数;虽然计算方式不同,但都与斜率值参数偏离0的程度呈正比。

-

当λ值不断增大时,惩罚项的权重不断增高;从而导致通过缩小斜率参数值使得损失函数总值下降的收益就越大。

- 换言之考虑惩罚项下降的强度与RRS项增高的强度,此时斜率参数值越接近0越好;

- 考虑到LASSO回归与岭回归形状的不同,LASSO能够将小的参数值缩小至0,即在模型中删除该变量,从而实现了特征选择的目的。

(2)弹性网络#

弹性网络中同时包含L2与L1正则化,通过α参数控制L2范数和L1范数的权重。所以在弹性网络中会有两个超参数。

如下公式

$$

J_{Net} = \sum_{i=1}^n(y_i-\hat{y_i})^2 + \lambda { (1-\alpha)\sum_{j=1}^p{\beta_j^2} + \alpha \sum_{j=1}^p{|\beta_j|} }

$$

2、mlr建模#

- 示例数据:小麦年产量

- 目的:根据第1~9列的预测变量信息预测小麦的产量

- 根据mlr包提供的"regr.glmnet"方法,进行三种正则化建模。

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

|

library(mlr)

data(Iowa, package = "lasso2")

iowaTib <- Iowa

head(iowaTib)

# Year Rain0 Temp1 Rain1 Temp2 Rain2 Temp3 Rain3 Temp4 Yield

# 1 1930 17.75 60.2 5.83 69.0 1.49 77.9 2.42 74.4 34.0

# 2 1931 14.76 57.5 3.83 75.0 2.72 77.2 3.30 72.6 32.9

# 3 1932 27.99 62.3 5.17 72.0 3.12 75.8 7.10 72.2 43.0

# 4 1933 16.76 60.5 1.64 77.8 3.45 76.4 3.01 70.5 40.0

# 5 1934 11.36 69.5 3.49 77.2 3.85 79.7 2.84 73.4 23.0

# 6 1935 22.71 55.0 7.00 65.9 3.35 79.4 2.42 73.6 38.4

##第10列为小麦的产量

##其余列为小麦生长不同阶段的天气情况

iowaTask <- makeRegrTask(data = iowaTib, target = "Yield")

|

2.1 岭回归#

2.1.1 确定训练方法#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

|

##(1)定义学习器

ridge <- makeLearner("regr.glmnet", alpha = 0)

# getParamSet(ridge)

# 默认对数据进行标准化,以避免不同尺度的斜率参数的差异影响

##(2)定义超参数空间:s即为λ,控制惩罚项的权重

ridgeParamSpace <- makeParamSet(

makeNumericParam("s", lower = 0, upper = 15))

##(3)随机搜索200个超参数

randSearch <- makeTuneControlRandom(maxit = 200)

##(4)10次重复的3折交叉验证

cvForTuning <- makeResampleDesc("RepCV", folds = 3, reps = 10)

|

2.1.2 选取最优超参数#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

|

library(parallel)

library(parallelMap)

parallelStartSocket(cpus = detectCores())

tunedRidgePars <- tuneParams(ridge, task = iowaTask, # ~30 sec

resampling = cvForTuning,

par.set = ridgeParamSpace,

control = randSearch)

parallelStop()

#最优超参数结果

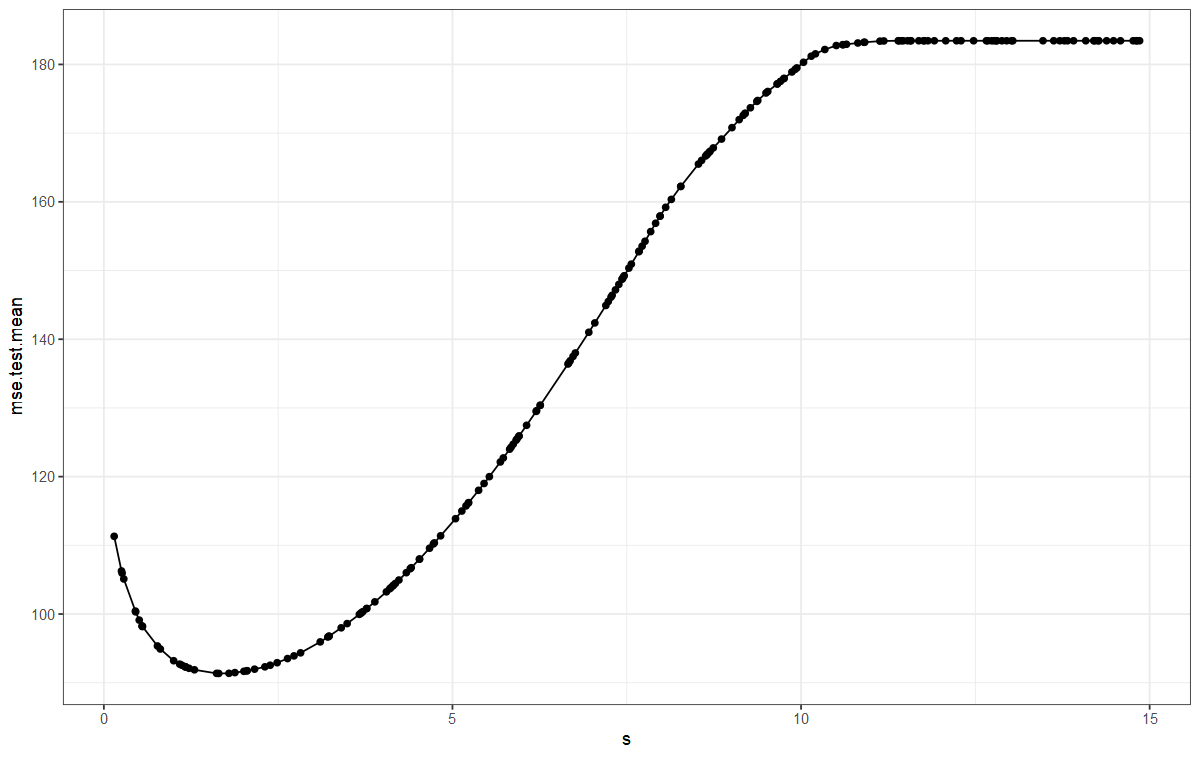

tunedRidgePars$x

#$s

#[1] 5.898183

#不同超参数结果可视化

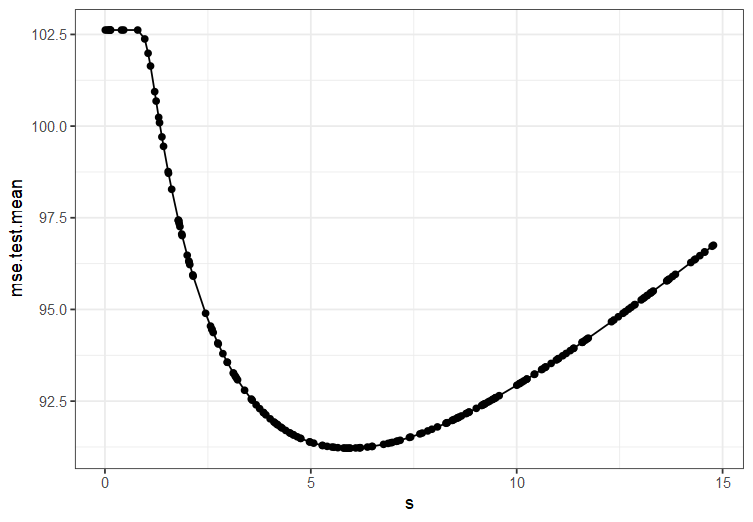

ridgeTuningData <- generateHyperParsEffectData(tunedRidgePars)

plotHyperParsEffect(ridgeTuningData, x = "s", y = "mse.test.mean",

plot.type = "line") +

theme_bw()

|

2.1.3 训练模型#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

|

##训练模型

tunedRidge <- setHyperPars(ridge, par.vals = tunedRidgePars$x)

tunedRidgeModel <- train(tunedRidge, iowaTask)

##查看模型结果

ridgeModelData <- getLearnerModel(tunedRidgeModel)

ridgeCoefs <- coef(ridgeModelData, s = tunedRidgePars$x$s)

ridgeCoefs

# 10 x 1 sparse Matrix of class "dgCMatrix"

# s1

# (Intercept) -916.65674179

# Year 0.53685059

# Rain0 0.34648992

# Temp1 -0.23854000

# Rain1 -0.70694968

# Temp2 0.03531768

# Rain2 1.92710185

# Temp3 -0.57686084

# Rain3 0.64050635

# Temp4 -0.47974939

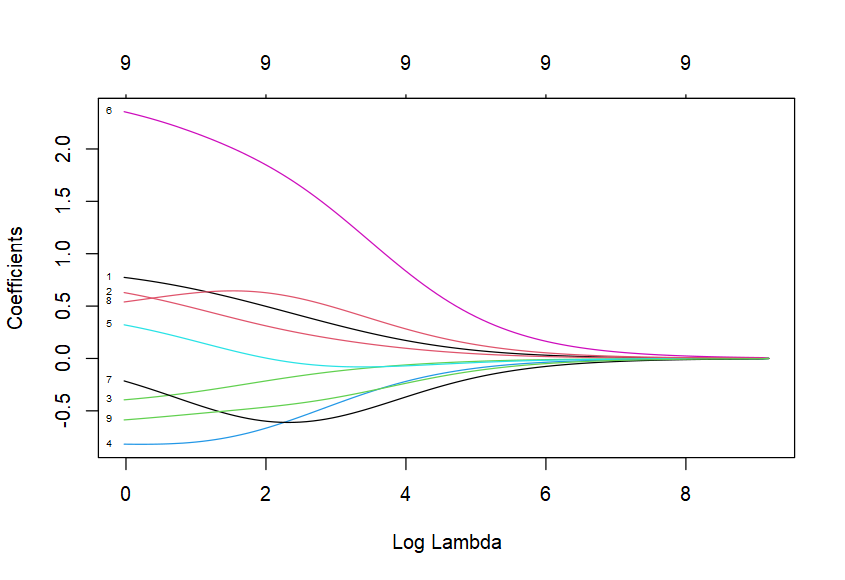

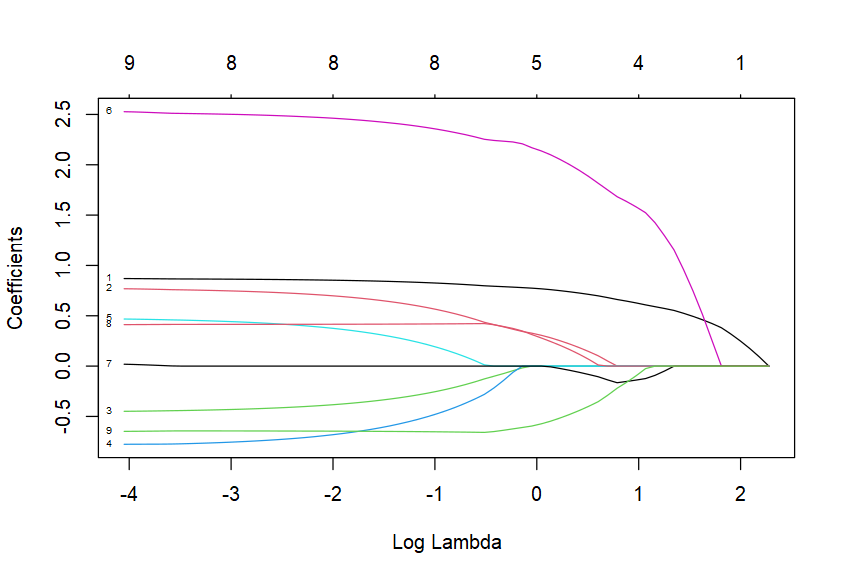

plot(ridgeModelData, xvar = "lambda", label = TRUE)

|

之前提及"regr.glmnet"会自动标准化,在计算斜率时则会自动转为变量原来的尺度。

2.2 lasso回归#

2.2.1 确定训练方法#

- 除了定义学习器时,alpha参数改为1,其它保持不变

1

2

3

4

5

6

7

8

9

10

11

12

13

14

|

##(1)定义学习器

lasso <- makeLearner("regr.glmnet", alpha = 1)

# getParamSet(lasso)

# 默认对数据进行标准化,以避免不同尺度的斜率参数的差异影响

##(2)定义超参数空间:s即为λ,控制惩罚项的权重

lassoParamSpace <- makeParamSet(

makeNumericParam("s", lower = 0, upper = 15))

##(3)随机搜索200个超参数

randSearch <- makeTuneControlRandom(maxit = 200)

##(4)10次重复的3折交叉验证

cvForTuning <- makeResampleDesc("RepCV", folds = 3, reps = 10)

|

2.2.2 选取最优超参数#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

|

library(parallel)

library(parallelMap)

parallelStartSocket(cpus = detectCores())

tunedLassoPars <- tuneParams(lasso, task = iowaTask, # ~30 sec

resampling = cvForTuning,

par.set = lassoParamSpace,

control = randSearch)

parallelStop()

#最优超参数结果

tunedLassoPars$x

#$s

#[1] 1.647296

#不同超参数结果可视化

lassoTuningData <- generateHyperParsEffectData(tunedLassoPars)

plotHyperParsEffect(lassoTuningData, x = "s", y = "mse.test.mean",

plot.type = "line") +

theme_bw()

|

2.2.3 训练模型#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

|

##训练模型

tunedLasso <- setHyperPars(lasso, par.vals = tunedRidgePars$x)

tunedLassoModel <- train(tunedLasso, iowaTask)

##查看模型结果

lassoModelData <- getLearnerModel(tunedLassoModel)

lassoCoefs <- coef(lassoModelData, s = tunedLassoPars$x$s)

lassoCoefs

# 10 x 1 sparse Matrix of class "dgCMatrix"

# s1

# (Intercept) -1.313315e+03

# Year 7.138660e-01

# Rain0 1.489506e-01

# Temp1 .

# Rain1 .

# Temp2 .

# Rain2 1.890166e+00

# Temp3 -8.095605e-02

# Rain3 7.292344e-02

# Temp4 -4.042185e-01

##如上有3个变量被剔除

plot(lassoModelData, xvar = "lambda", label = TRUE)

|

2.3 弹性网络#

2.3.1 确定训练方法#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

|

elastic <- makeLearner("regr.glmnet")

##(1)定义学习器

elastic <- makeLearner("regr.glmnet")

# getParamSet(elastic)

# 默认对数据进行标准化,以避免不同尺度的斜率参数的差异影响

##(2)定义超参数空间:s即为λ,控制惩罚项的权重

elasticParamSpace <- makeParamSet(

makeNumericParam("s", lower = 0, upper = 10),

makeNumericParam("alpha", lower = 0, upper = 1))

##(3)随机搜索400个超参数

randSearchElastic <- makeTuneControlRandom(maxit = 400)

##(4)10次重复的3折交叉验证

cvForTuning <- makeResampleDesc("RepCV", folds = 3, reps = 10)

|

2.3.2 选取最优超参数组合#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

|

library(parallel)

library(parallelMap)

parallelStartSocket(cpus = detectCores())

tunedElasticPars <- tuneParams(elastic, task = iowaTask, # ~30 sec

resampling = cvForTuning,

par.set = elasticParamSpace,

control = randSearchElastic)

parallelStop()

#最优超参数结果

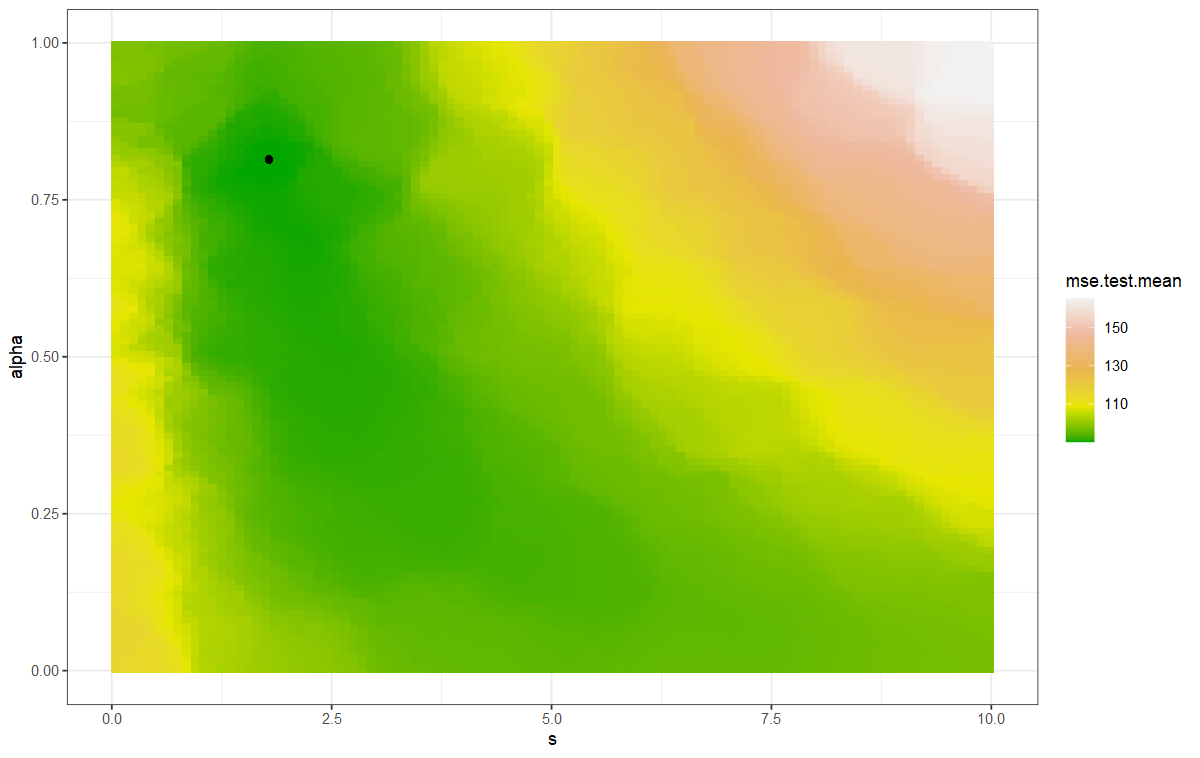

tunedElasticPars$x

#$s

#[1] 1.786091

#$alpha

#[1] 0.8142816

#不同超参数结果可视化

elasticTuningData <- generateHyperParsEffectData(tunedElasticPars)

plotHyperParsEffect(elasticTuningData, x = "s", y = "alpha",

z = "mse.test.mean", interpolate = "regr.kknn",

plot.type = "heatmap") +

scale_fill_gradientn(colours = terrain.colors(5)) +

geom_point(x = tunedElasticPars$x$s, y = tunedElasticPars$x$alpha) +

theme_bw()\

#如下图,黑点标注的即为最优超参数组合

|

2.3.3 训练模型#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

|

##训练模型

tunedElastic <- setHyperPars(elastic, par.vals = tunedElasticPars$x)

tunedElasticModel <- train(tunedElastic, iowaTask)

##查看模型结果

elasticModelData <- getLearnerModel(tunedElasticModel)

elasticCoefs <- coef(elasticModelData, s = tunedElasticPars$x$s)

elasticCoefs

# 10 x 1 sparse Matrix of class "dgCMatrix"

# s1

# (Intercept) -1290.1150312

# Year 0.7038625

# Rain0 0.1786434

# Temp1 .

# Rain1 .

# Temp2 .

# Rain2 1.9443047

# Temp3 -0.1234248

# Rain3 0.1621764

# Temp4 -0.4266126

##如上同样有3个变量被剔除

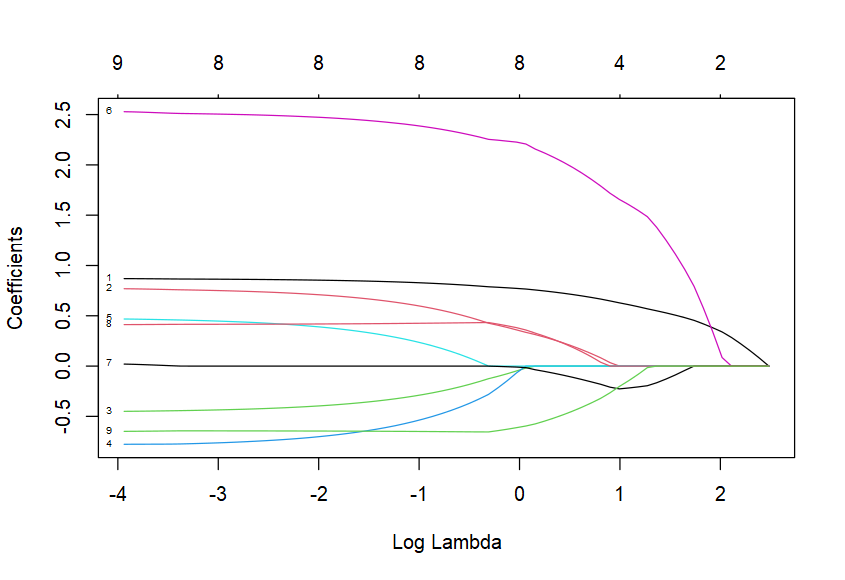

plot(elasticModelData, xvar = "lambda", label = TRUE)

|

2.4 对比三个模型结果#

2.4.1 预测变量系数比较#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

|

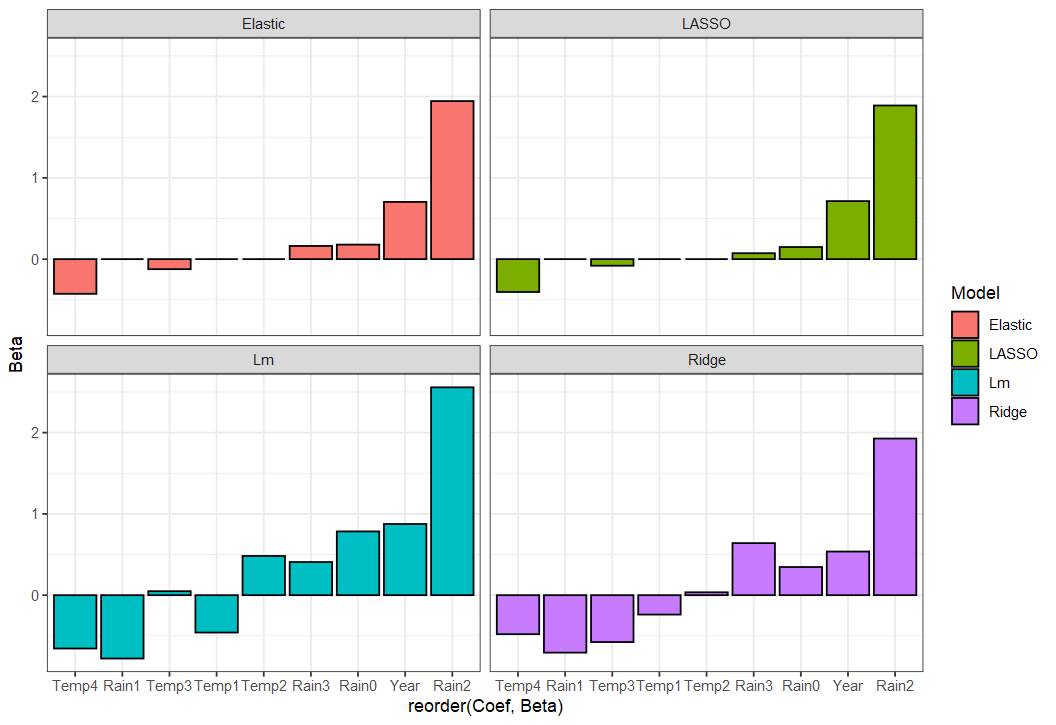

#(1)普通线性回归

lmCoefs <- coef(lm(Yield ~ ., data = iowaTib))

#(2)岭回归

coefTib <- tibble(Coef = rownames(ridgeCoefs)[-1],

Ridge = as.vector(ridgeCoefs)[-1],

Lm = as.vector(lmCoefs)[-1])

coefUntidy <- gather(coefTib, key = Model, value = Beta, -Coef)

#(3)lasso回归

coefTib$LASSO <- as.vector(lassoCoefs)[-1]

coefUntidy <- gather(coefTib, key = Model, value = Beta, -Coef)

#(4)弹性网络

coefTib$Elastic <- as.vector(elasticCoefs)[-1]

coefUntidy <- gather(coefTib, key = Model, value = Beta, -Coef)

ggplot(coefUntidy, aes(reorder(Coef, Beta), Beta, fill = Model)) +

geom_bar(stat = "identity", position = "dodge", col = "black") +

facet_wrap(~ Model) +

theme_bw()

|

2.4.2 benchmark#

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

|

##(1)初始化模型

ridge <- makeLearner("regr.glmnet", alpha = 0, id="ridge")

ridgeWrapper <- makeTuneWrapper(ridge, resampling = cvForTuning,

par.set = ridgeParamSpace,

control = randSearch)

lasso <- makeLearner("regr.glmnet", alpha = 0, id="lasso")

lassoWrapper <- makeTuneWrapper(lasso, resampling = cvForTuning,

par.set = lassoParamSpace,

control = randSearch)

elastic <- makeLearner("regr.glmnet", alpha = 0, id="elastic")

elasticWrapper <- makeTuneWrapper(elastic, resampling = cvForTuning,

par.set = elasticParamSpace,

control = randSearchElastic)

learners = list(ridgeWrapper, lassoWrapper, elasticWrapper, "regr.lm")

##(2)开始测试

library(parallel)

library(parallelMap)

kFold3 <- makeResampleDesc("CV", iters = 3)

parallelStartSocket(cpus = detectCores())

bench <- benchmark(learners, iowaTask, kFold3)

parallelStop()

bench

# bench

# task.id learner.id mse.test.mean

# 1 iowaTib ridge.tuned 204.6557

# 2 iowaTib lasso.tuned 209.6984

# 3 iowaTib elastic.tuned 179.3852

# 4 iowaTib regr.lm 251.6789

|